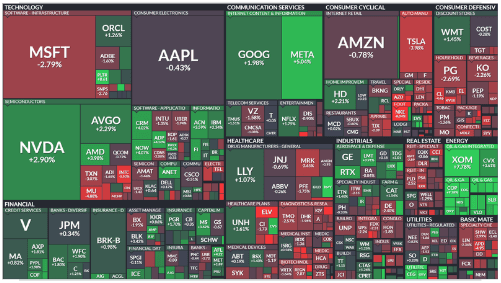

Weekly Market Recap:

This week, U.S. equities were slightly higher, with the S&P 500 gaining +0.22%, the Dow up +0.09%, and the Nasdaq rising +0.10%, marking a fourth straight week of gains for the S&P and Nasdaq. The Russell 2000 underperformed, slipping -0.54%.

Key performers included CVS (+5.2%) in the drugstore/PBM sector and NVDA (+2.9%) as AI demand remained strong. However, NKE (-8%) and TSLA (-4%) lagged amid concerns in the athletic apparel and EV sectors.

Sectors that outperformed included energy (+7.01%), communication services (+2.20%), and utilities (+1.09%). Materials (-1.98%) and real estate (-1.88%) were among the underperformers. Treasury yields rose, the dollar strengthened (+2.1%), while gold was mostly flat. Crude oil surged +9.1%, the biggest weekly gain since March 2023, on geopolitical tensions in the Middle East.

Corporate Highlights:

NVDA (+2.9%) saw strong demand for its Blackwell chips.

NKE (-8%) pulled FY25 guidance due to a CEO transition and missed Q1 sales expectations.

TSLA (-4%) dropped on weaker-than-expected Q3 deliveries.

LEVI (-8.5%) lowered FY revenue guidance after missing sales estimates.

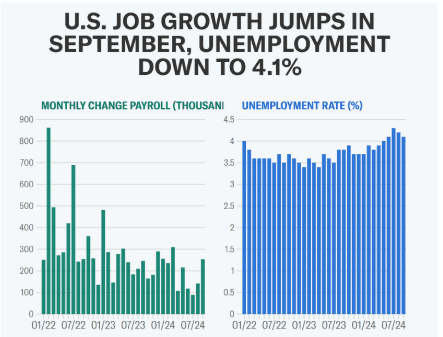

The September jobs report has delivered a strong dose of optimism for the U.S. economy, with a surprising 254,000 jobs added, far surpassing the 150,000 expected by economists. The unemployment rate ticked down to 4.1%, further solidifying the labor market’s resilience. In a time when many anticipated signs of economic cooling, this report reaffirms the underlying strength of U.S. employment. Wage growth, another key indicator, climbed to 4% year-over-year, suggesting that inflationary pressures remain intact. While the Federal Reserve has been cautious about cutting interest rates further, this robust job growth complicates the narrative. Many analysts had hoped for more evidence of economic deceleration to justify further rate cuts, but Friday’s report challenges that outlook. This stronger-than-expected labor market also bolstered equity markets, with futures on major indices rallying post-report. The S&P 500, Dow Jones, and Nasdaq all saw gains, as the data offered renewed confidence in continued economic expansion. However, the Fed is now faced with a conundrum: how to balance robust economic growth with its goal of controlling inflation. With hopes for a large rate cut fading, the central bank may be forced to rethink its approach as it navigates the delicate dance of economic policy.

Next Week:

Notable Earnings:

Tuesday (10/8)

PepsiCo ($PEP)

Saratoga Investment ($SAR)

Wednesday (10/9)

Applied Digital Corporation ($APLD)

Helen of Troy ($HELE)

AZZ ($AZZ)

Thursday (10/10)

Delta Air Lines ($DAL)

Domino's Pizza ($DPZ)

Progressive ($PGR)

Friday (10/11)

JPMorgan Chase & Co. ($JPM)

Wells Fargo ($WFC)

BlackRock ($BLK)

Notable Ex-Dividend Date:

Monday (10/7)

Edison International ($EIX) 3.63%

McCormick & Company, Incorporated ($MKC) 2.01%*

Tuesday (10/8)

Dollar General ($DG) 1.91%

Roper Technologies, Inc. ($ROP) 0.50%

Vail Resorts, Inc. ($MTN) 4.90%

Wednesday (10/9)

Mastercard Incorporated ($MA) 0.50%

The Gap, Inc. ($GAP) 3.04%

Thursday (10/10)

AT&T Inc. ($T) 5.10%

Delta Air Lines, Inc. ($DAL) 1.28%

General Mills, Inc. ($GIS) 3.25%*

Friday (10/11)

General Dynamics Co. ($GD) 1.97%

American Eagle Outfitters, Inc. ($AEO) 2.42%

*Dividend Aristocrat