Weekly Market Recap:

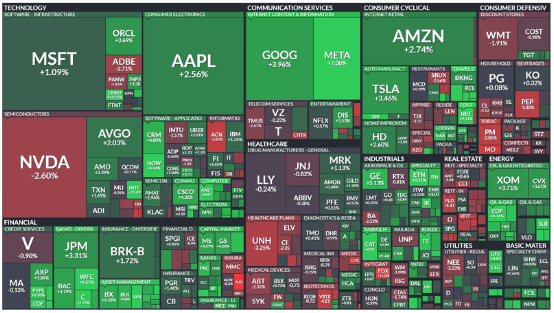

This week, U.S. equities saw notable gains, with the S&P 500 hitting a new all-time high and closing up +3.50%. The Dow rose +2.60%, the Nasdaq climbed +4.02%, and the Russell 2000 increased +4.36%. The rally followed the Federal Reserve’s dovish pivot, which surprised markets with a 50 basis point rate cut. Key performers included META (+7.0%) and banks, while NVDA dipped -2.6%.

Sectors that outperformed included energy (+3.79%), communication services (+3.70%), and financials (+2.35%). Underperformers were real estate (-1.31%) and consumer staples (-1.24%). Treasury yields were mixed, and the dollar weakened against the euro and pound but strengthened against the yen. Gold reached a record high, up +1.4%, while crude oil prices rose +3.4%. Next week’s focus will be on flash PMIs and earnings reports from MU and COST.

Corporate Highlights

LUNR (+49.3%) secured a significant NASA contract.

CEG (+30.1%) signed a long-term power purchase agreement with Microsoft.

FDX (-11.1%) missed earnings expectations and lowered guidance.

PGNY (-31.2%) faced a major client termination, impacting revenue.

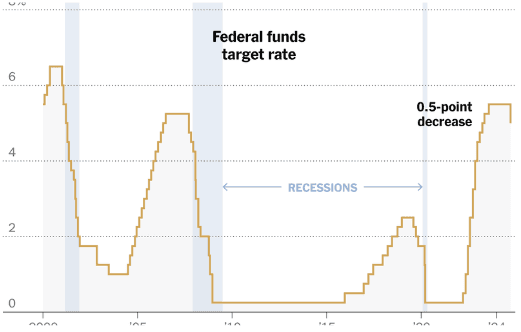

In a pivotal move, the Federal Reserve has cut interest rates by 50 basis points for the first time since the onset of the pandemic, signaling a shift in monetary policy amidst evolving economic indicators. This decisive action reflects the Fed’s growing confidence that inflation is stabilizing closer to its 2% target, even as signs of a softening labor market emerge. The 11-1 vote underscores a rare dissent, illustrating the complexity of the current economic landscape. Chair Jerome Powell's commitment to balancing inflation control with employment stability is commendable. However, this aggressive cut raises questions about the long-term implications for the economy. While a cut can stimulate growth, it risks igniting inflation if not carefully managed. Besides for the 2020 emergency cuts, the last significant reduction occurred in 2008 during the financial crisis, making this context particularly sensitive. Moreover, the Fed’s decision is likely to influence global central banks, as many await cues from the U.S. The ripple effects of this policy shift could alter investment strategies worldwide. Investors must remain vigilant; as the Fed recalibrates its approach, market volatility may persist. The balancing act of fostering growth while avoiding a resurgence of inflation remains a delicate dance, one that will require astute navigation in the coming months.

Next Week:

Notable Earnings:

Monday (9/23)

Red Cat Holdings Inc. ($RCAT)

AAR Corp. ($AIR)

Tuesday (9/24)

AutoZone Inc. ($AZO)

Stitch Fix Inc. Cl A ($SFIX)

Wednesday (9/25)

Micron Technology Inc. ($MU)

Cintas Corp. ($CTAS)

Thursday (9/26)

Costco Wholesale Corp. ($COST)

Accenture PLC Cl A ($ACN)

CarMax Inc. ($KMX)

BlackBerry Ltd. ($BB)

Notable Ex-Dividend Dates:

Monday (2/26)

Eversource Energy ($ES) 4.24%

Seagate Technology Holdings plc ($STX) 2.56%

W. R. Berkley Co. ($WRB) 0.60%

Tuesday (2/27)

Equity Residential ($EQR) 3.50%

Wednesday (2/28)

Johnson Controls International ($JCI) 2.10%

Thursday (2/29)

General Electric ($GE) 0.62%

Philip Morris International Inc. ($PM) 4.31%

Build-A-Bear Workshop, Inc. ($BBW) 2.69%

Friday (3/1)

Danaher Co. ($DHR) 0.39%

Nucor Co. ($NUE) 1.54%*

Keurig Dr Pepper Inc. ($KDP) 2.48%

*Dividend Aristocrat