Weekly Market Recap:

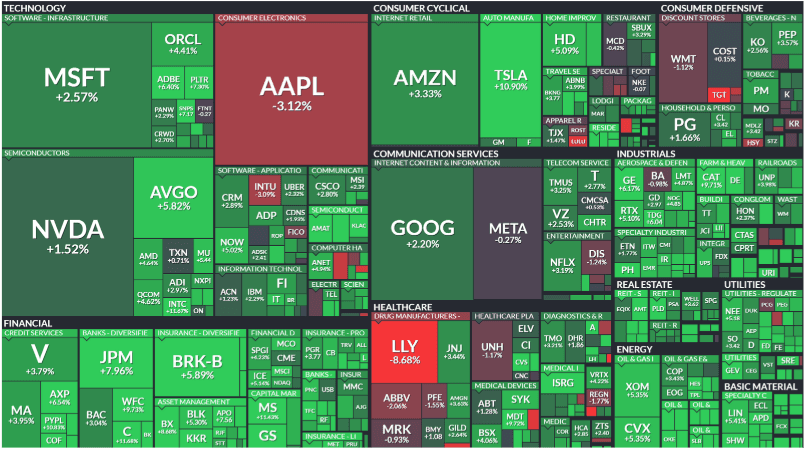

This week, U.S. equities posted strong gains across the board. The Dow (+3.69%), S&P 500 (+2.91%), Nasdaq (+2.45%), and Russell 2000 (+3.96%) all ended higher, reversing recent declines. Outperformers included banks, homebuilders, energy, and industrial metals. Relative laggards were pharma, biotech, managed care, and staples retailers. Treasuries were firmer, with the 30Y yield retreating after hitting 5%. The dollar index dipped (-0.3%), while Bitcoin jumped +10.8% back above $100K. Gold rose +1.2%, and WTI crude climbed +1.1%.

Corporate Highlights:

JPMorgan Chase (JPM +8.2%): Strong trading and credit results; raised 2025 NII guidance.

Wells Fargo (WFC +10.2%): Mixed results; robust NII guidance.

Morgan Stanley (MS +11.7%): EPS and revenue beat; equities trading excelled.

Goldman Sachs (GS +11.8%): Outperformed in FICC and equity; strong underwriting results.

United Rentals (URI +14.9%): Acquiring H&E Equipment Services (+100.6%).

Eli Lilly (LLY -9.3%): Missed guidance; weak drug uptake.

Sector Performance:

Outperformers included Energy (+6.14%), Financials (+6.10%), and Materials (+6.01%), while Healthcare (+0.30%), Consumer Staples (+1.26%), and Communication Services (+1.31%) lagged.

With bullish sentiment driven by disinflation progress, strong Q4 earnings from banks, and improving breadth, investor focus now shifts to next week’s inauguration and potential policy clarity under the new administration.

The Medicare price negotiation program is poised to reshape the cost landscape for weight-loss drugs like Ozempic and Wegovy, marking a pivotal moment in U.S. healthcare policy. Starting in 2027, prices for these blockbuster medications, currently priced at $12,000 to $16,000 annually, are expected to drop significantly. This shift comes as the government, under the Inflation Reduction Act, works to balance innovation with accessibility. While these negotiations promise potential savings for Medicare, they also spark broader implications. Lower prices could ripple across the industry, forcing competing drugs, like Eli Lilly’s Zepbound, to follow suit. As pharmacy benefit managers gain leverage, private insurers may also benefit, potentially reducing costs for millions of Americans. However, the anticipated expansion of Medicare coverage to include weight-loss drugs for a wider audience could offset savings, increasing overall federal expenditure despite reduced per-patient costs. The upcoming Trump administration faces critical decisions. While price cuts align with the promise of affordable healthcare, the balance between cost reductions and fostering pharmaceutical innovation will be challenging. Further, Robert F. Kennedy Jr., as the incoming health secretary, adds uncertainty, given his mixed views on these drugs and drug company practices. As the policy unfolds, its success will hinge on careful negotiation and implementation. The stakes are high, not just for the pharmaceutical industry but for millions of Americans grappling with the high costs of obesity treatments.

Next Week:

Notable Earnings:

Monday (1/20)

MARKET CLOSED (MLK Day)

Tuesday (1/21)

Netflix, Inc. ($NFLX)

The Charles Schwab ($SCHW)

Capital One Financial ($COF)

Wednesday (1/22)

Procter & Gamble Company ($PG)

Johnson & Johnson ($JNJ)

Progressive Corporation ($PGR)

Thursday (1/23)

Texas Instrument Incorporated ($TXN)

GE Aerospace ($GE)

Friday (1/24)

American Express ($AXP)

Verizon ($VZ)

Notable Ex-Dividend Dates:

Monday (1/20)

MLK Day

Tuesday (1/21)

Caterpillar ($CAT) 1.45%*

Colgate ($CL) 2.16%*

Zoetis ($ZTS) 1.12%

Wednesday (1/22)

Dell Technologies ($DELL) 1.42%

Lowe’s Companies ($LOW) 1.71%*

Thursday (1/23)

CVS Health ($CVS) 6.02%

Friday (1/24)

Albertsons Companies ($ACI) 3.05%

Banco Santander ($BSBR) 5.10%

Coca-Cola Consolidated ($COKE) 0.80%

Procter & Gamble ($PG) 2.52%*

Pfizer ($PFE) 6.78%

Pentair ($PNR) 0.90%

*Dividend Aristocrat