Weekly Market Recap:

U.S. equities posted gains this week, with the Dow (+0.55%), S&P 500 (+1.47%), and Nasdaq (+2.58%) all advancing, while the Russell 2000 (+0.01%) was flat. The Nasdaq outperformed, fueled by strong gains in Big Tech, including Nvidia (+6.9%) and Apple (+7.5%). Other leaders included semiconductors, China tech, steel, and casinos, while laggards included managed care, airlines, regional banks, and credit cards. Treasuries were firmer, the dollar index declined (-1.2%), gold set a new record high (+0.5%), and WTI crude edged lower (-0.3%).

Corporate Highlights:

Apple (AAPL +7.5%): Announced AI partnership with Alibaba to boost iPhone capabilities in China.

Coca-Cola (KO +7.9%): Surpassed organic growth expectations by over 700 basis points.

CVS (CVS +21.8%): Surged on a strong Q4 earnings beat.

Airbnb (ABNB +19.6%): Delivered strong growth in gross booking value and nights booked.

DraftKings (DKNG +26.5%): Raised FY25 revenue guidance.

Trade Desk (TTD -31.6%): Missed expectations for the first time in over 30 quarters.

Sector Performance:

Outperformers: Tech (+3.76%), Communication Services (+1.98%), Materials (+1.75%).

Underperformers: Healthcare (-1.11%), Financials (+0.08%), Industrials (+0.15%).

Markets focused on AI deals, Trump’s tariff developments, and hotter-than-expected CPI data. Investors now turn to next week’s FOMC minutes, housing data, and major earnings from Walmart, Booking Holdings, and Occidental Petroleum.

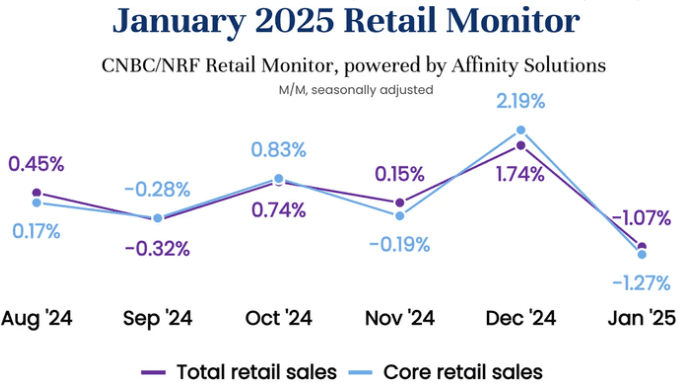

Consumer spending took an unexpected hit in January, with retail sales falling 0.9%, far worse than the 0.2% decline economists had anticipated. This downturn, reported by the Commerce Department, follows a strong 0.7% gain in December, signaling potential economic headwinds for the first quarter of 2025. The decline was broad-based, with sporting goods, online retailers, and auto sales seeing the biggest drops. Excluding autos, retail sales still fell 0.4%, missing expectations for a modest increase. Even the control group metric, which factors into GDP calculations, slipped 0.8%, raising concerns about economic growth. Some analysts caution against overreacting, pointing to factors such as bad weather and December’s auto sales boom, which was driven by dealer incentives. Despite the weak January figures, consumer spending overall remains stable due to strong wage growth and a resilient labor market. Inflation remains another challenge. While consumer prices rose 0.5% in January, the producer price index showed some signs of easing. Meanwhile, import prices surged 0.3%, their largest jump since April 2024, with fuel costs rising even more. The unexpected retail slump has fueled speculation that the Federal Reserve may cut interest rates sooner than expected, with June emerging as a possible timeline. Investors and policymakers will be watching closely to determine whether this is a temporary dip or an early warning of broader economic weakness.

What to watch:

Notable Earnings-

Monday (2/17)

Otter Tail Corp. ($OTTR)

Huntsman Corp. ($HUN)

Tuesday (2/18)

La-Z-Boy Inc. ($LZB)

MasterBrand Inc. ($MBC)

Wednesday (2/19)

Wix.com Ltd. ($WIX)

Fiverr International Ltd. ($FVRR)

Garmin Ltd. ($GRMN)

Wingstop Inc. ($WING)

Thursday (2/20)

Hasbro Inc. ($HAS)

Shake Shack Inc. Cl A ($SHAK)

Friday (2/21)

Oil States International Inc. ($OIS)

Notable Ex-Dividend Dates:

Tuesday (2/18)

Capital One Financial ($COF) 1.18%

Ford Motor ($F) 6.40%

Johnson & Johnson ($JNJ) 3.43%*

Prudential Financial ($PRU) 4.80%

Wednesday (2/19)

Aflac ($AFL) 2.08%*

Consolidated Edison ($ED) 3.69%*

Thursday (2/20)

Applied Materials ($AMAT) 0.95%

Discover Financial Services ($DFS) 1.41%

Microsoft ($MSFT) 0.77%

Friday (2/21)

BP ($BP) 5.50%

Cummins ($CMI) 1.96%*

Equifax ($EFX) 0.58%

Hilton Worldwide ($HLT) 0.22%

*Dividend Aristocrat