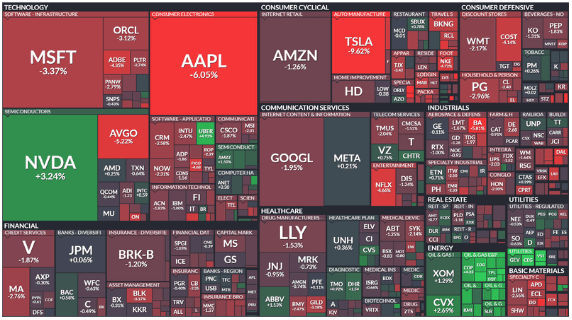

Weekly Market Recap:

This week, U.S. equities had a mixed performance to kick off 2025. The Dow (-0.60%), S&P 500 (-0.48%), and Nasdaq (-0.51%) posted declines, while the Russell 2000 (+1.06%) outperformed. Key outperformers included energy, semis, REITs, utilities, and managed care, while laggards were auto retailers, airlines, software, and industrial metals. Treasuries firmed, and the yield curve steepened. The dollar index rose +0.9%, while gold gained +0.8%, and WTI crude jumped +4.7%.

Corporate Highlights:

Tesla (TSLA -4.9%): Missed Q4 deliveries, marking its first y/y delivery decline in over a decade.

Apple (AAPL -4.7%): Announced a four-day iPhone discount in China amid reports of steep y/y shipment declines.

Fannie Mae (FNMA +79.3%) & Freddie Mac (FMCC +74.7%): Surged after the FHFA and Treasury revealed plans to end conservatorships.

Rivian (RIVN +20.8%): Beat Q4 production and delivery estimates.

Amazon (AMZN +0.2%) & Lyft (LYFT +7.2%): Reports suggested a potential acquisition by Amazon in 2025.

Boeing (BA -5.9%): Pressured by a 737-800 crash in South Korea.

Sector Performance:

Top performers included Energy (+3.24%) and Utilities (+1.32%), while Materials (-2.09%) and Consumer Discretionary (-1.46%) lagged. Markets are eyeing key data next week, including December payrolls and PMI, along with FOMC minutes, for clues on the Fed’s next steps amid a cautiously optimistic economic outlook.

The U.S. auto industry closed 2024 with a 2.7% increase in new vehicle sales, signaling a promising rebound despite persistently high prices and interest rates. Over 16 million vehicles were sold, the highest since 2019, reflecting cautious optimism among consumers as the average price edged slightly downward, and borrowing costs began to ease. Electric vehicles (EVs) continued to grow, with sales rising 8.8% to nearly 1.3 million units, albeit at a slower pace than 2023’s 47% surge. Meanwhile, hybrid vehicles gained traction with a remarkable 36% increase, showcasing a consumer shift toward diverse energy options amid fluctuating fuel prices and regulatory uncertainty. The looming possibility of the new administration scrapping EV tax credits adds to the uncertain future of electrification. Among automakers, General Motors led with a 4.3% sales boost, while Ford and Toyota followed closely. However, Stellantis struggled with a 14.8% drop, underscoring the impact of high inventories and premium pricing. Buyers looking for deals may find opportunities with brands like Stellantis or Ford, which have greater availability compared to supply-constrained Honda and Toyota. With two Federal Reserve rate cuts expected this year and rising manufacturer discounts, especially on 2024 models, the second half of 2025 may offer significant relief to buyers. For those willing to wait and remain flexible, the automotive market’s gradual normalization promises a brighter and more affordable future.

Next Week:

Notable Earnings:

Monday (1/6)

Commercial Metals Co. ($CMC)

Tuesday (1/7)

AAR Corp. ($AIR)

Cal-Maine Foods Inc. ($CALM)

Wednesday (1/8)

Albertsons Cos. Inc. ($ACI)

PriceSmart Inc. ($PSMT)

Acuity Brands Inc. ($AYI)

Thursday (1/9)

Simply Good Foods Co. ($SMPL)

KB Home ($KBH)

Friday (1/10)

Delta Air Lines Inc. ($DAL)

Tilray Brands Inc. ($TLRY)

Walgreens Boots Alliance Inc. ($WBA)

Notable Ex-Dividend Dates:

Monday (1/6)

JPMorgan Chase & Co. ($JPM) 2.05%

Owens Corning ($OC) 1.38%

Tuesday (1/7)

Dollar General ($DG) 2.96%

Landstar System ($LSTR) Special Dividend of $2.00/share

Wednesday (1/8)

Comcast ($CMCSA) 2.84%

GAP ($GAP) 2.74%

Thursday (1/9)

Oracle ($ORCL) 0.90%

Friday (1/10)

AT&T ($T) 4.75%

General Mills ($GIS) 3.80%*

Intuit ($INTU) 0.70%

Mastercard ($MA) 0.57%

*Dividend Aristocrat