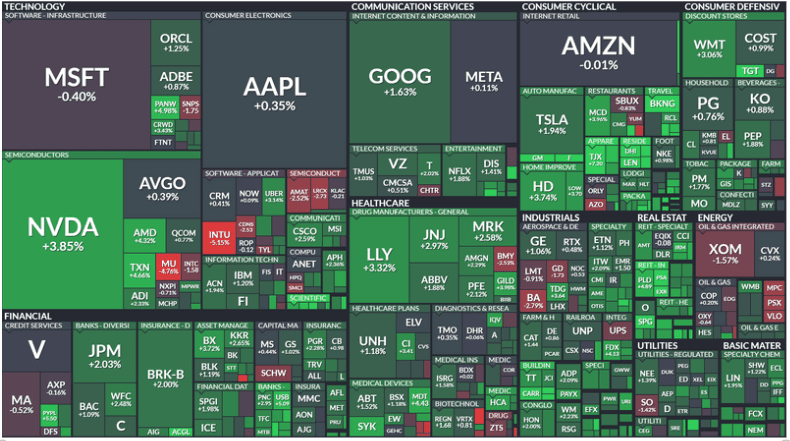

Weekly Market Recap:

U.S. equities closed higher, with the Dow up 1.14%, S&P 500 up 1.15%, and Nasdaq gaining 1.47%. The Russell 2000 led the charge with a 3.19% increase. These gains reversed Thursday's declines, with the S&P 500 and Nasdaq posting their second straight week of gains, bringing the S&P within 1% of a record close.

Gold hit a fresh all-time high, up 1.2%, while Bitcoin surged 5.6%. WTI crude rose 2.5% despite a weekly decline.

Notable Gainers:

Cava Group (CAVA) +19.6%

Workday (WDAY) +12.5%

Warby Parker (WRBY) +11.9%

Notable Decliners:

Intuit (INTU) -6.8%

Bill Holdings (BILL) -6.7%

GE Vernova (GEV) -1.5%

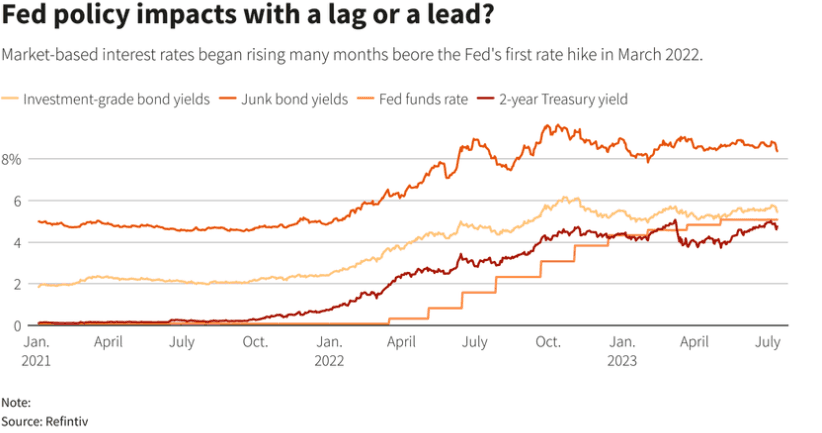

Federal Reserve Chair Jerome Powell’s recent remarks at the Jackson Hole summit mark a significant turning point in monetary policy. With inflation finally easing after a prolonged battle, Powell’s declaration that “the time has come for policy to adjust” signals a shift from aggressive rate hikes to potential cuts in the near future. For over two years, the Fed's primary focus has been taming inflation, which reached its highest levels in over four decades. Eleven rate hikes between March 2022 and July 2023 have succeeded in cooling the economy, with inflation now edging closer to the Fed’s 2% target. Yet, Powell’s speech also emphasized that the labor market remains robust, albeit with rising unemployment due to increased workforce participation.

The market's reaction was swift, with stocks gaining and Treasury yields dropping as traders priced in the likelihood of a rate cut as early as September. Powell, however, refrained from providing a definitive timeline, leaving the door open for adjustments based on incoming data. As we look ahead, the Fed’s dual mandate—balancing price stability with full employment—will continue to guide its actions. Powell’s cautious optimism reflects confidence in the Fed’s ability to navigate these challenges, but the path forward remains uncertain. Investors should brace for a new phase of monetary policy, one that promises to be just as dynamic as the last.

Next Week:

Notable Earnings:

Monday (8/26)

PDD Holdings Inc. ADR (PDD)

BHP Group Ltd. ADR (BHP)

Tuesday (8/27)

Bank of Montreal (BMO)

Bank of Nova Scotia (BNS)

Nordstrom Inc. (JWN)

Wednesday (8/28)

Salesforce Inc. (CRM)

NVIDIA Corp. (NVDA)

HP Inc. (HPQ)

Thursday (8/29)

Dell Technologies Inc. Cl C (DELL)

Ulta Beauty Inc. (ULTA)

Lululemon Athletica Inc. (LULU)

Friday (8/30)

JinkoSolar Holding Co. Ltd. ADR (JKS)

Industrial & Commercial Bank of China Ltd. ADR (IDCBY)

Notable Ex-Dividend Dates:

Monday (8/26)

3M (MMM) 2.20%

Nathan’s Famous (NATH) 2.75%

Tuesday (8/27)

Hyatt Hotels (H) 0.45%

Johnson & Johnson (JNJ) 3.28%

Wednesday (8/28)

Electronic Arts (EA) 0.51%

Thursday (8/29)

Home Depot (HD) 2.50%

WK Kellogg (KLG) 3.68%

Friday (8/30)

Avangrid (AGR) 4.97%

eBay (EBAY) 1.92%

DuPont de Nemours (DD) 1.90%

*Dividend Aristocrat